We've done this before.

http://frscalls.blogspot.com/2009/10/advertisement-for-financial-research.html That was a straight copy from our website at frs.transmatch.com

This time let's show what FRS can do. Remember you have access to just about everything you will need for quantitative analysis of the stock market's movements since 1974. You have all Ford Equity variables for every member of the S&P500 when they were in the index. And most importantly the data are hardwired into Tableau software. That means anyone with ideas but lousy technical skills (e.g. me) can begin to test theories and measure performance in minutes.

First we'll look at Aug. 2007-Oct.2009. Lots happened. Maybe to much too comprehend. I heard a BarCap quant describing the period as one of constant regime change. I don't see that. Quite simply everything sold off at about equal speed until March of this year when they bought the junk (high beta low VMO). That trend stayed in place until October and now we are adrift. The biggest surprise was how unsafe you were with a safe portfolio in late 2008. The selling was indiscriminate. We also ran a backtest that showed that since forever it's been a better idea to own stocks that had gone up in the preceding year rather than ones that had gone down. Crude? Simplistic? Sure but that the strategy of buying price momentum worked over time. But not since March of this year as you can see. Also note that Ford's VMO indicator worked much better that plain old beta.

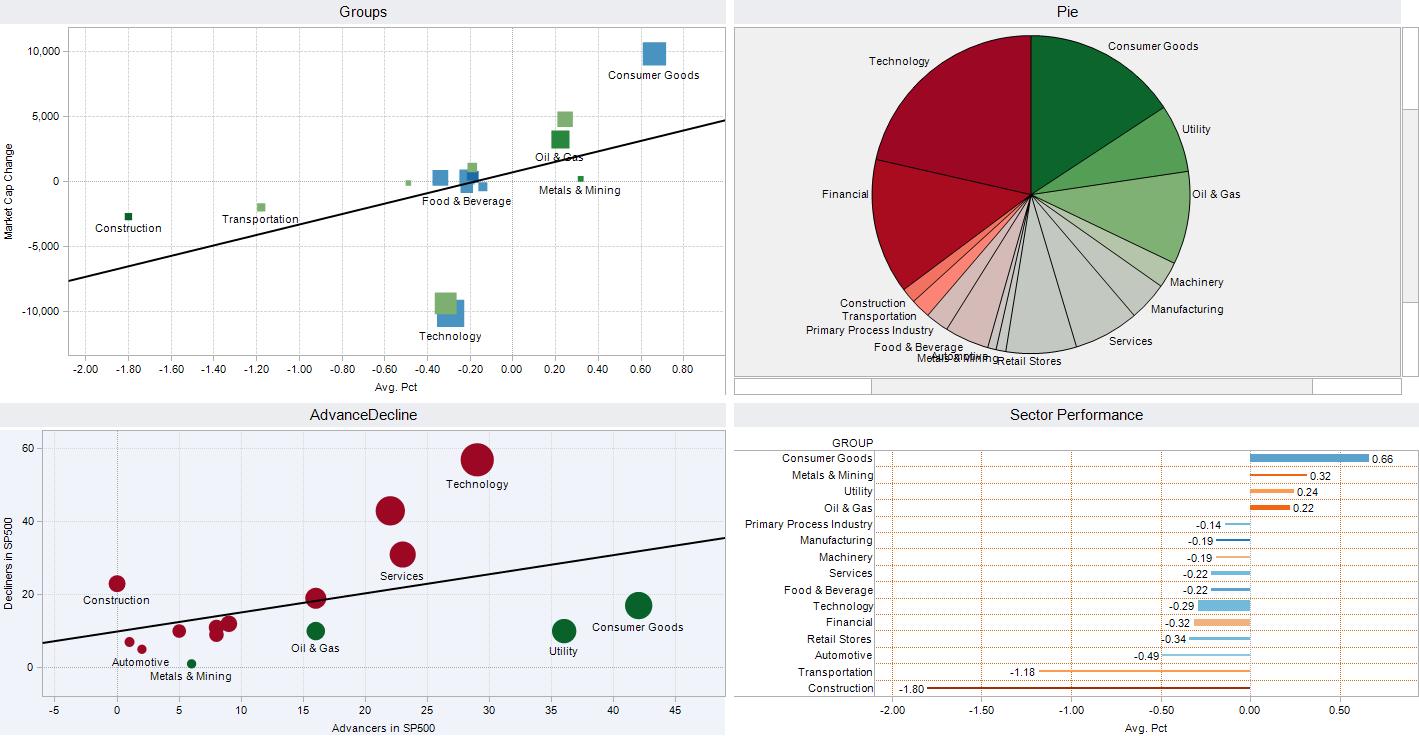

Now using the same model but with a slightly shorter time frame viz. October. Which was a bad month. High risk names measured any which way did not do well. High risk fund managers suffered the torments of the beta bear. Isn't it strange how all the "stockpickers" who did well this summer did poorly in October? You can see the best performing stocks as of 10/30 for the preceding three months. The colors indicate whether the stocks were high or low VMO (quality). With FRS you can visually analyze several variables in the same chart. Last you can see which industries did best or worst in October. The trend line says that no matter what you did if you had a high beta portfolio you were hurt.

Those are a few of the things I pulled from the FRS model this afternoon. Perhaps you can see a bias towards the way I look at the market. k. But you can do the same thing with FRS. Bring your own theory of the market and test it out. Value? Momentum? Earnings Surprise? Mean Reversion? Long-Short? You can test your biases in a blink with FRS. It's what you do when you find out that

everything you know is wrong that will make the difference.